Practice A

- Credit Score

- 760

- DSCR

- 1.45

- Net Income

- Supports debt service

- PDI

- 97, Strong

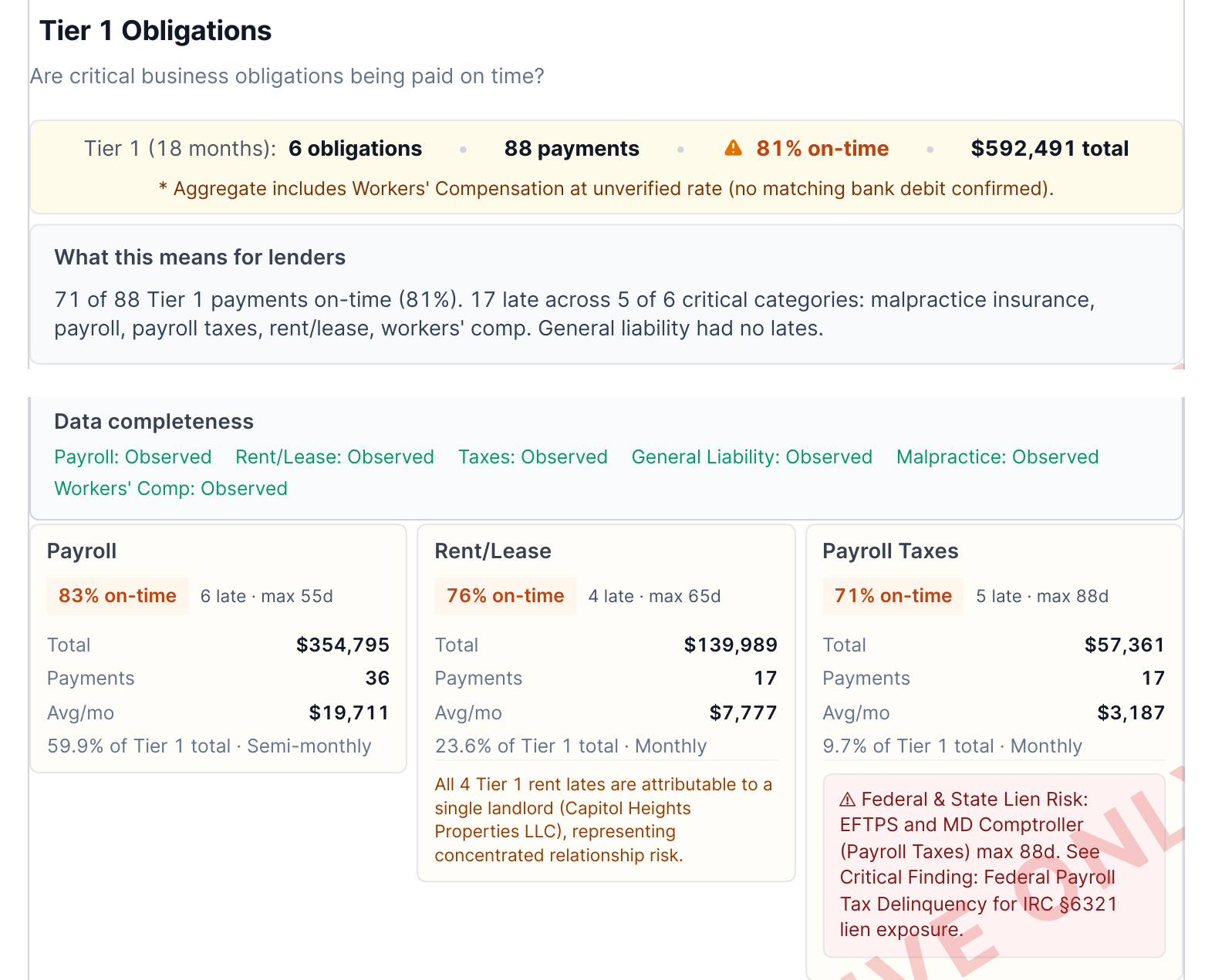

Payroll, taxes, rent, and vendors paid within terms across 18 months.

Independent Underwriting Intelligence for Healthcare Lenders

For healthcare lenders, SBA 7(a), CDFI & equipment finance teams

Credeity gives lenders independent visibility into how healthcare practices manage recurring obligations, receivables, and payment behavior, from first underwrite through the life of the loan.

Financial statements show what a borrower says is happening. Payment behavior shows what is actually happening (behavioral intelligence).

Traditional underwriting tells you whether repayment appears possible. Credeity shows how borrowers actually behave before problems appear.

| You already review | What it doesn't reveal | What Credeity adds |

|---|---|---|

| Credit bureau report | How vendors actually get paid | Payment Discipline Index (PDI) |

| Tax returns | Payment behavior between filing periods | Multi-month payment trend |

| Financial statements | Operational discipline month to month | Cash flow corroboration |

| Bank statements | Payment prioritization under stress | Payment prioritization analysis |

| AR aging | Vendor-side payment stretch | Collection deterioration signal |

| Practice production | Revenue quality and collection consistency | Collection consistency signals |

| Credit references | Recurring payment discipline | Cross-source payment reconciliation |

Every Underwriting Intelligence Report combines evidence no single source provides.

How the practice actually pays payroll, payroll taxes, rent, and key vendors, verified from borrower-authorized records and scored as a Payment Discipline Index.

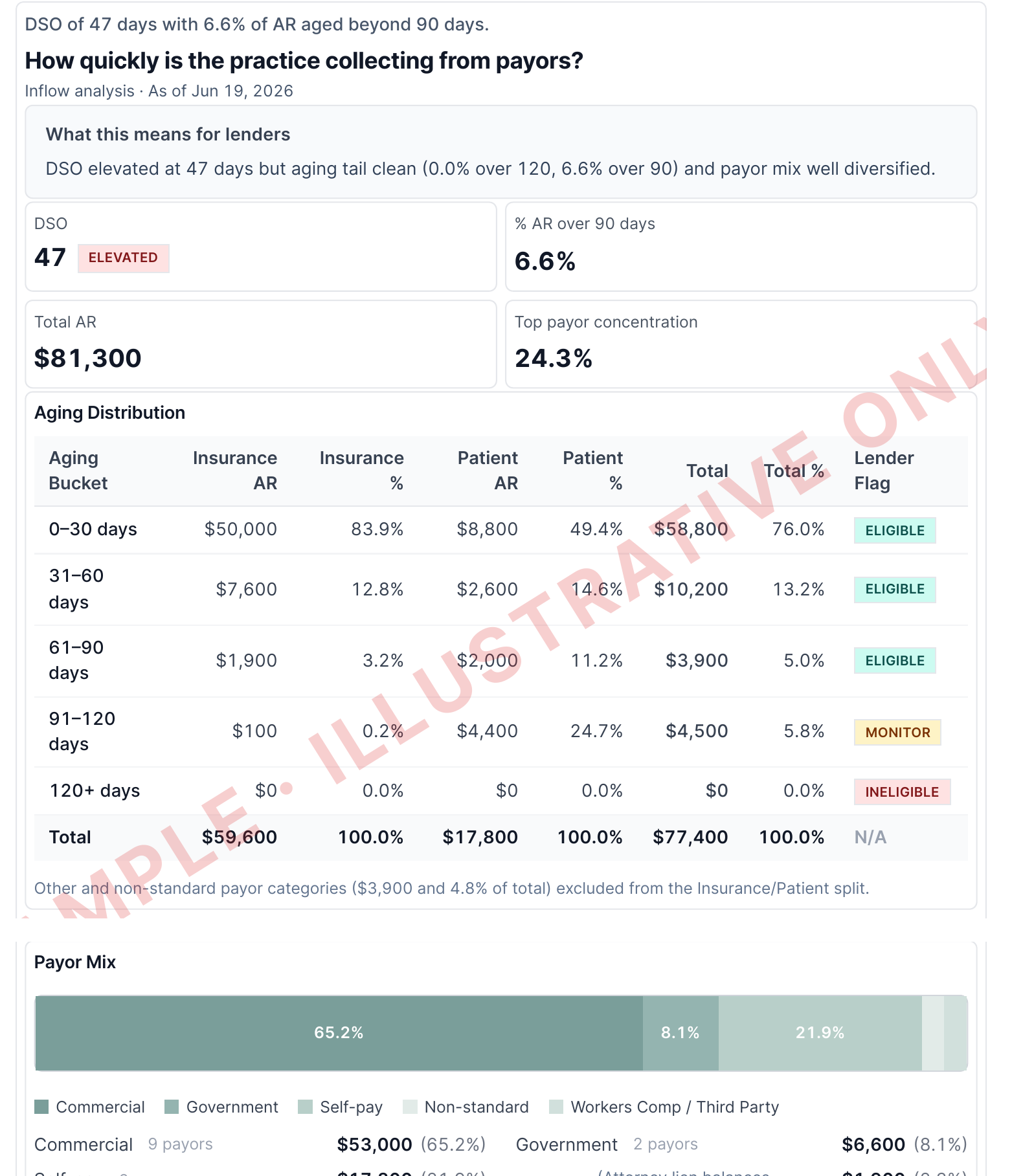

Collection trends, days sales outstanding against practice-type benchmarks, and payor concentration that shapes repayment capacity.

UCC filings, tax transcripts, and license checks documented alongside the behavioral analysis in Comprehensive engagements.

Payroll, taxes, rent, and vendors paid within terms across 18 months.

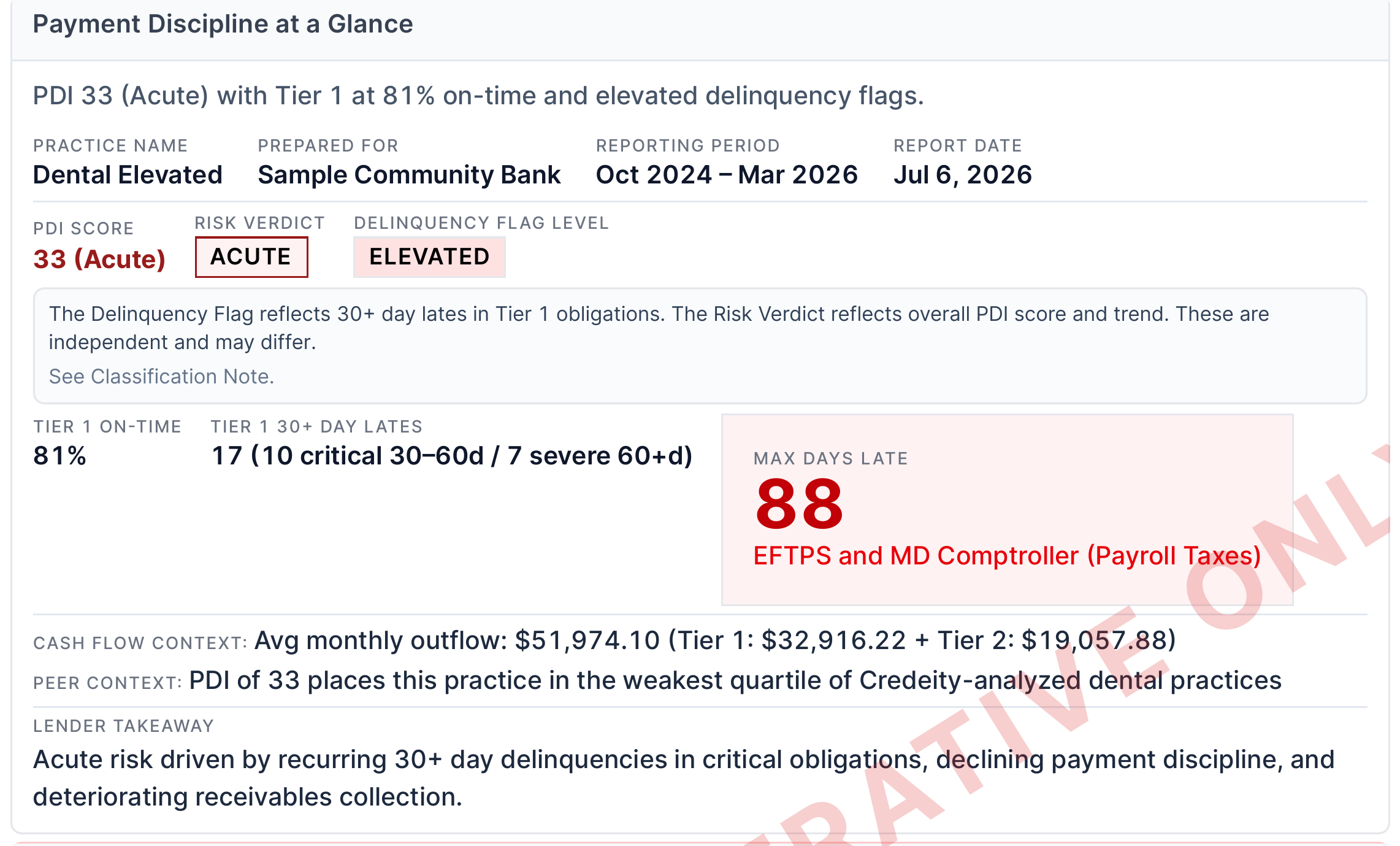

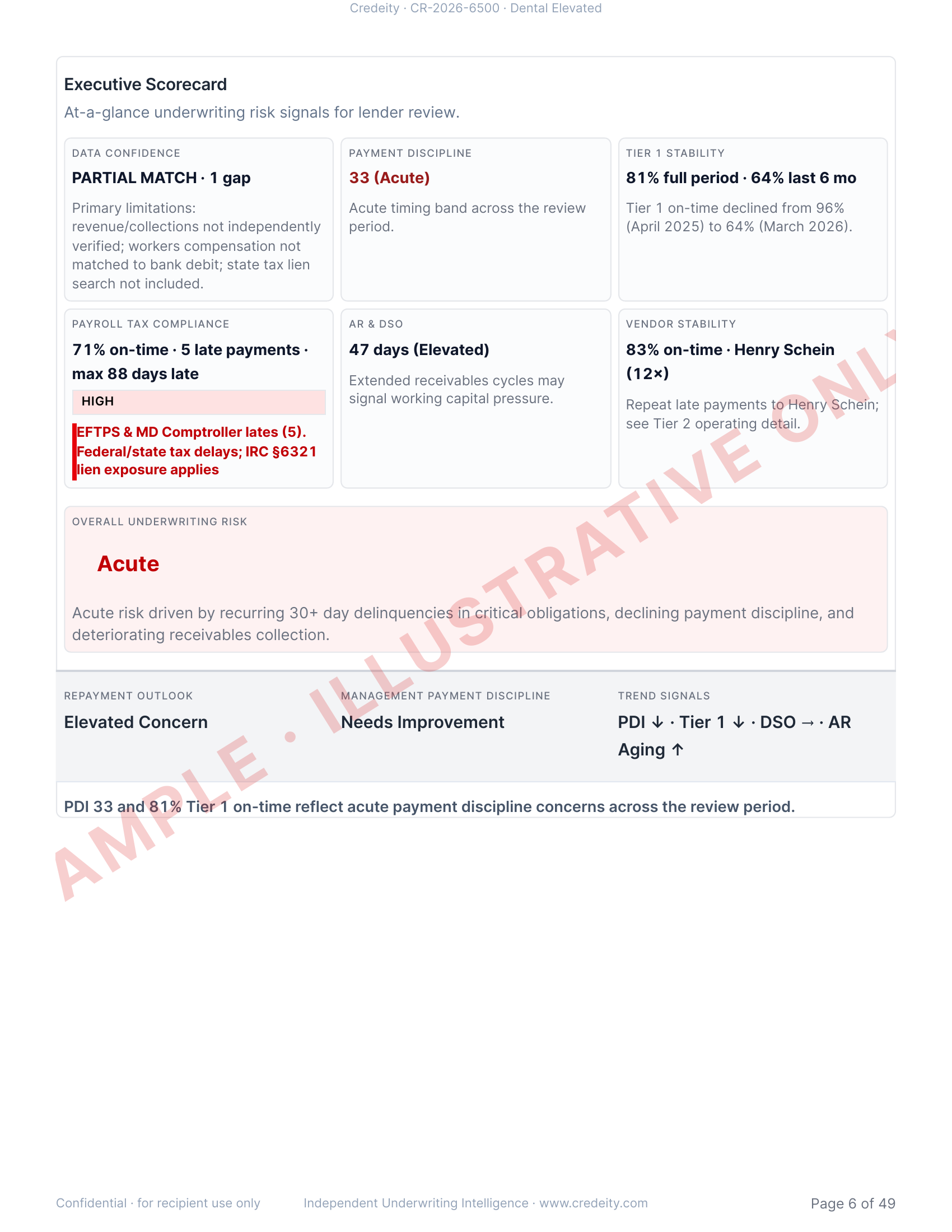

Repeated payroll tax delays. Medical suppliers stretched past 45 days. Payment discipline declining over the review period.

Clean bureau. DSCR above policy. Financials current. Recommend approval.

Federal payroll taxes paid up to 88 days late. Workers' Compensation payments unverified against bank records. Medical suppliers repeatedly stretched. PDI declined from 96 to 33 over the review period.

Outcome: conditional approval, with tax compliance verified before closing and quarterly monitoring as a covenant. Same borrower, better-informed decision.

Credeity provides behavioral analytics as a supplemental input to underwriting. Lenders make and own every credit decision.

A second, independent underwriting source (second-look underwriting) layered on your existing process. No system replacement, no infrastructure overhaul.

Credeity gives lenders a structured view of borrower payment behavior and receivables performance using borrower-authorized operating data. It is designed to complement, not replace, the diligence tools banks already use, including tax transcripts, UCC and lien searches, commercial bureau reports, license verification, and other third-party checks.

Credeity helps lenders see what standard documents often miss: how a healthcare practice manages recurring obligations like payroll, taxes, rent, insurance, and critical vendors over time. The result is a clearer underwriting file, stronger exception support, and better documentation when the credit story is not obvious from tax returns alone.

Trade data is voluntary, incomplete, and lagged. It does not show how a practice pays payroll and vendors. It does not show how it collects from payors. Bank statements confirm what happened. Accounting exports show why: which obligations were met, which slipped, and in what order.

Obligation-level payment discipline: payroll, taxes, rent, insurance, and vendors. Sourced from bill payment history, not bureau trade lines.

Receivables health: aging distribution, DSO vs practice-type benchmarks, payor mix, and concentration risk. Available before you underwrite repayment capacity.

Automated analysis. Analyst verified. Delivered in 48 hours.

Open a case in the Lender Portal and enter the borrower's contact.

The borrower signs the authorization and uploads accounting exports and bank statements. We confirm the submission is complete before analysis begins, so the clock starts on a full file.

Ingestion, reconciliation, benchmark comparison, and Payment Discipline Index scoring run as a rules-based pipeline. The same inputs always produce the same score.

A credentialed analyst reviews every exception, verifies the findings, and signs the report. Release requires a second review. No report ships on automation alone.

The full report arrives in your portal within 48 hours of a complete submission. Rush delivery in 24 hours is available.

Report documentation supports examiner inquiry, annual review files, and credit committee presentations.

Two of the pages lenders review first. Select either page to view at full resolution.

Illustrative report pages using synthetic borrower data.

Executive Scorecard - At-a-glance risk signals with PDI and overall underwriting rating

Payment Performance Trends - 18-month payment discipline across critical obligations

A strong file at origination can deteriorate within two quarters. Credeity Monitor re-scores the borrower's payment behavior monthly against a standing authorization, flags Payment Discipline Index movement, and alerts you immediately when a tax obligation goes more than 30 days past due. Write it into the loan covenants and the renewal takes care of itself.

See Credeity MonitorPriced like the third-party underwriting inputs you already use. Standardize Core across new practice credits; reserve Comprehensive for higher-risk and higher-stake exposures.

| Core | Comprehensive | Credeity Monitor | |

|---|---|---|---|

| Price | $1,500per case | $2,250per case | $3,600–$6,000per borrower per year ($300–$500 / month) |

| Designed for | The standard for new healthcare practice credits. Independent payment behavior analysis that reduces underwriting surprises and strengthens committee memos. | For larger exposures, exceptions, and higher-risk segments. Payment behavior analysis plus external validations, documented together in one report. | Continuous payment behavior monitoring for funded loans, written into the covenants. Monthly monitoring summaries, immediate alerts on tax slippage and PDI band changes, and a standing portfolio dashboard. |

| Includes |

| Everything in Core, plus an External Validation panel: UCC and lien searches, IRS payroll tax transcript status, and professional license verification. | |

| Data sources | Borrower-authorized accounting exports with optional bank statement reconciliation. | Core data sources plus lender-obtained external checks summarized in a standardized panel. | |

| See Credeity Monitor |

The standard for new healthcare practice credits. Independent payment behavior analysis that reduces underwriting surprises and strengthens committee memos.

Data sources

Borrower-authorized accounting exports with optional bank statement reconciliation.

For larger exposures, exceptions, and higher-risk segments. Payment behavior analysis plus external validations, documented together in one report.

Data sources

Core data sources plus lender-obtained external checks summarized in a standardized panel.

Continuous payment behavior monitoring for funded loans, written into the covenants. Monthly monitoring summaries, immediate alerts on tax slippage and PDI band changes, and a standing portfolio dashboard.

Credeity combines rules-based underwriting methodology with analytical automation to structure borrower-authorized accounting data into consistent, lender-ready intelligence. Credit decisions remain entirely under lender control.

Portal access is provisioned within one business day. Existing lenders sign in directly.